Expert Contributors

Bob Collins

Read More

Kaitlyn Tracy

Read More

TYPES OF LOANS FOR GRADUATE STUDENTS

The student loan debt crisis is real. Today’s students owe an average loan debt of about $23,000, with graduate students averaging about of $50,000. In this guide, prospective graduate students can learn how to utilize student loan options, including repayment plans and loan forgiveness programs, without acquiring exorbitant debt.

This section describes the types of graduate student loans, including the interest rates that are generally applied.

Stafford loans are supplied to graduate students by the U.S. Department of Education. These loans are given out on an unsubsidized basis, which means they begin to accrue interest immediately while the borrowers are completing their degree programs.

The interest rates that are applied to Stafford loans depend on when the student borrows money. In 2013, the federal government passed legislation that sets these student loan interest rates at the same amount as the 10-year Treasury note, which can change from year to year.

For example, students who took out loans in the 2013-2014 school year had an interest rate set at 5.41 percent, which is locked in for the life of the loan.

Graduate students who take out Stafford loans can borrow up to $20,500 annually. Students should keep in mind however that the federal government caps the amount that they can borrow at $138,500 — an amount that includes any funding they may have borrowed during their undergraduate years. Additionally, those studying in certain health fields lifetime loan amount is capped at $224,000.

Also offered by the federal government, Graduate PLUS loans can be borrowed by students who want to use the funds to not only pay their tuition and fees, but also reasonable living expenses. However, unlike Stafford loans, students who apply for this funding must pass a credit check and can be denied if they have undergone a bankruptcy or have accounts that are in collections.

The interest rates of Graduate PLUS loans are also determined by the interest of 10-year Treasury notes.

Students with a high financial need may be qualified to take out Perkins loans, which are funded by the federal government and administered through their college or university. Students are able to borrow $8,000 per year, with a lifetime limit of $40,000, including undergraduate funding.

The interest rates of Perkins loans are set at 5 percent for the life of the loan, and interest does not begin to accrue until nine months after borrowers have finished their degree programs.

Private loans are the funding that students receive from lending institutions outside of the federal government. These loans can be a lot riskier, as their interest rates are variable and can fluctuate throughout the length of the loan.

For example, an institution may offer an interest rate as low as 2.25 percent when the student first borrows the money, but that amount can increase at any time — putting students in a position where they owe much more than they originally bargained for when they began their graduate programs. Some private lenders will fix their interest rates, which can amount to rates lower than federal loans in some cases.

When taking out private loans for graduate school, it’s imperative that students understand the terms so they know exactly what they’re signing up for. These loans can amount to a significant financial obligation, so students must always read the fine print before signing on the dotted line.

The U.S. Department of Education has useful resources that can help students evaluate the different types of loans. However, depending on your creditworthiness, a private student loan from your bank or credit union may offer competitive interest rates. Be sure to compare the repayment plans and consider the generous deferment, forbearance, and loan forgiveness options that federal loans offer.

Bob Collins, Bob Collins, VP Financial Aid, Western Governors UniversityUndergraduate and

Graduate Student Loans: Know the Difference

Just like education itself, student loans for graduate and undergraduate students are not the same. The following table includes some differences between graduate and undergraduate student loans.

| Graduate | Undergraduate | ||

|---|---|---|---|

| Interest accrual | The interest on federal student loans for graduate students begins to accrue immediately after taking out the loan. | Federal student loans are unsubsidized, so interest does not begin to accrue until after the student has graduated. | |

| Loan amount | Since the tuition rates for graduate school are generally much higher than those for undergraduate studies, it’s not surprising that the amount students at this level can borrow from the federal government is also higher. Most graduate students can borrow up to $20,500 in Stafford loans per year, while those in medical school may get $40,500 annually. |

The cap on undergraduate Stafford loans depends on how far students are in their degree programs. The breakdown is currently as follows:

The total amount that undergraduates are allowed to borrow is $31,000. |

|

| Interest rates | Interest rates for graduate students are higher. In the 2013-2014 academic year, the rate was 6.21 percent. | Interest rates for undergraduate students are lower. In the 2013-2014 academic year, the rate was 4.66 percent. | |

| Needs-based aid | Needs-based federal loans are available to graduate students, but on a much smaller scale. | There are more opportunities for undergraduates to receive needs-based loans, depending on their family income levels. | |

| Deferment | Graduate students can defer their loans, but they have to specifically make a request. | Student loans are automatically deferred while undergraduate students are in school. |

Coralee

Coralee is a graduate student going to school to become an advanced nurse. She needs to borrow $40,000 in student loans for her graduate education, in addition to her $10,000 in undergraduate loans.

BEST LOAN OPTIONCoralee would be better off getting a federal student loan.

EXPLANATIONAs a nurse, Coralee will have the opportunity to participate in a federal loan forgiveness program. In exchange for working at a facility affected by the nationwide nursing shortage, her loan will be wiped out after a certain number of payments.

Trent

Trent is a graduate student studying business. During his research, he found a private lender that offers a fixed interest rate of 2.5 percent. He has always heard federal loans are better so he’s uncertain if he should get this type of loan.

BEST LOAN OPTIONTrent would be better off getting a private loan.

EXPLANATIONWhile the interest rates of federal loans are generally lower than those of private lenders, in this case, a fixed rate of 2.5 for the duration of the loan would be less than what he would receive from a Stafford loan.

A STEP-BY-STEP LOOK AT THE

STUDENT LOAN APPLICATION PROCESS

When students apply for graduate school, they take painstaking care to ensure that the applications are filled out accurately and completely. When they apply for student loans, they should be just as diligent.

Here’s a step-by-step overview of the application process for graduate student loans.

Fill out a Free Application for Federal Student Aid (FAFSA®)

Fill out a Free Application for Federal Student Aid (FAFSA®)

The first step to receiving graduate school loans is to fill out the FAFSA®. This application is designed to give the federal government information to determine the types and amounts of financial aid that students are eligible to receive—including scholarships, grants, and loans. In order to do this, the form asks for information about students’ income, and how much money they have in personal savings and investment accounts.

FAFSA® forms can be found at fafsa.ed.gov. Application deadlines may differ from state to state, so the site allows students to search for their applicable due dates. Since federal loans are in high demand, it's important for students to get their applications in as soon as possible.

Review financial aid award letter

Review financial aid award letter

After analyzing students’ financial data, the U.S. Department of Education issues a financial aid award letter outlining how much they can receive in scholarships, grants, and loans. This allows students to make decisions about whether or not they need to supplement their federal financial aid with a private loan, or find other ways of funding their education.

Contact financial aid office

Contact financial aid office

After reviewing the information in the award letter, student should contact their school to formally accept the financial aid being offered and arrange to fill out paperwork associated with their federal loan.

Apply for additional loans as needed

Apply for additional loans as needed

If the financial aid that students receive from their grants, scholarships, and federal loans is not enough to pay for their education, and they have no other sources of funding, they should put in an application with a private lender for additional loans. After shopping around for the best loan option, students should follow a specific lender’s application process.

Receiving funding

Receiving funding

Loans are paid directly to the students’ college or university, which applies the money to tuition and fees. Whatever is left over is refunded directly to students.

It is important for students to understand when interest will begin accruing on their loan, and the interest rate and fees that the lender charges. It is also important for students to routinely monitor their lifetime loans, so they are always aware of how much student debt they accrued. Students can monitor their federal loan amounts through the National Student Loan Directory Service.

Kaitlyn Tracy, Director of Admissions, Spring Arbor University

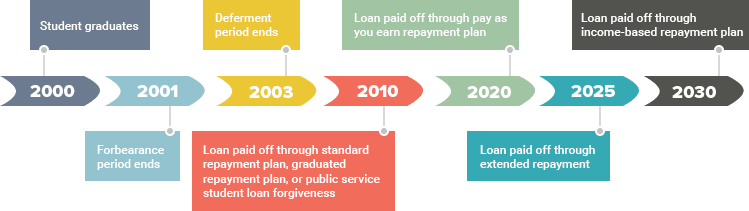

Repayment Timeline

While many students may dream of winning the lottery and paying off the balance of their student loan in one fell swoop, the reality is usually much different. That doesn’t mean graduates have to be shackled to their student loan for the rest of their lives; there are several payment options that students can choose from, some of which can help speed up the repayment process.

The following gives a glimpse of how these payment plans work.

Repayment Plans Explained

Forbearance

Time Period:1 year

A temporary postponement that graduates can receive if they are unable to make loan payments. Interest continues to accrue during this time.

Deferment

Time Period:3 years

A temporary postponement that borrowers can receive if they are unemployed, returning to school, suffering from a disability, or serving in the military. Unsubsidized loans accrue interest during this time, while subsidized loans do not.

Standard Repayment Plan

Time Period:10 years

Students make monthly payments on a regular schedule. Minimum payment amounts are calculated based on a 10-year period.

Graduated Repayment Plan

Time Period:10 years

Students make lower payments than those on the regular schedule. Every two years, the minimum payment amount increases.

Public Service Student Loan Forgiveness

Time Period:10 years

Students who hold certain jobs in the public sector—including government agencies, the military, and non-profit and public service organizations—may be able to have the balance of their loans forgiven after making payments for 10 years.

Pay As You Earn Repayment Plan

Time Period:20 years

Monthly payments do not exceed 10 percent of the borrower’s discretionary income. As the graduate’s income changes, the payments change. After 20 years of successful payments, the loan balance is forgiven.

Extended Repayment Plan

Time Period:25 years

Allows students to extend the life of their loan in order to make lower monthly payments.

Income-Based Repayment Plan

Time Period:30 years

Monthly payments are based on income. Some of the loan may be forgiven after an extended amount of time.

Avoiding Loan Default

Repaying student loans can often be challenging, especially in a bad economy, but it’s imperative that graduates do what they can to keep their payments up to date.

Students who have not made payments on their loans for 270 to 360 days, and have not made arrangements with the lender to postpone payments, will have their accounts moved into default status.

The consequences of this are serious, and can include being referred to a collections agency, getting sued for the entire loan amount, and having employment wages garnished. In addition, graduates whose loans are in default may be prohibited from joining the military or renewing professional licenses.

It doesn’t have to get to this extreme point, however. Some strategies to prevent defaulting on student loans include borrowing only as much as needed, applying for a forbearance or deferment when a temporary financial hardship arises, and exploring alternative repayment options.

Q&A: University Vice President of Financial Aid

Bob Collins, VP Financial Aid, Western Governors University

Why should a prospective student consider taking out student loans?

Students should only consider loans after exhausting all other resources such as personal savings, school payment plans, employer tuition benefits, and scholarships. The cost of higher education is an investment in yourself — the more you borrow, the higher the cost, lowering your return on investment. If you have to borrow money, apply the income tax savings, if any, as a lump sum payment toward the principal balance of your student loan.

What advice do you offer graduate students about paying for school and taking out loans?

First, do your homework. Even before looking at loans, students should research and consider costs at different universities. For example, tuition and fees at online universities vary widely, from approximately the same cost as public universities to more than twice as much. Higher cost does not necessarily mean higher quality, so be sure to understand all of the costs—tuition, books, and fees.

Another factor in your cost consideration should be the length of time you expect to take to complete your degree—the longer it takes, the more it is likely to cost. Some universities, such as WGU, combine a flat-rate tuition with a competency-based model, which allows students to advance as soon as they demonstrate mastery of course materials, making it possible for many students to accelerate their progress toward a degree, saving both time and money.

If a student needs to take out a loan, it is best to borrow only the amount needed for unmet direct costs (tuition and fees after other resources are applied), rather than borrowing the maximum amount allowed.

What are some mistakes that students make when taking out loans for their education?

Mistake #1:

Not understanding the total repayment cost over the life of the loan (principal plus interest over 10 or more years).

Mistake #2:Borrowing the annual maximum. This is a bad idea. Be frugal to optimize your return on investment. Borrow only what you need to cover the unmet direct costs (tuition and fees after other resources are applied). Live within your means and pay your indirect costs (living expenses) with job wages, savings, and investments.

UNDERSTANDING LOAN FORGIVENESS

Public Service Reduces Student Loan Debt

Those in public service fields find their jobs rewarding because they get the opportunity to give back to the community. But there is one reward that they may not be aware of: the Public Service Loan Forgiveness Program, or PSLF. Under this program, graduates who work for qualified employers on a full-time basis are able to have their loans forgiven after making 120 consecutive payments.

10 Loan Forgiveness Facts You Need to Know

-

Who are qualified public service workers?

Qualified workers are those who are employed by a public service organization approved by the program. These employers include:

-

Federal, state, local, and tribal government agencies

-

Private not-for-profit organizations that provide services to the public, such as emergency management, law enforcement, education, library, and public health services

-

Tax-exempt not-for-profit organizations with 501(c)(3) status

-

-

How are full-time employees defined?

For PSLF purposes, full-time employment is defined by whatever the employer considers that status to be, or 30 hours per week, whichever is greater.

-

What federal loans are covered by PSLF?

Subsidized and unsubsidized Stafford, Direct PLUS, and Federal Direct Consolidation loans are covered by PSLF.

-

Are private loans eligible to be forgiven by PSLF?

Students with private and other non-federal loans are ineligible to receive PSLF benefits.

-

What is a qualified monthly payment?

Any payments that are made after October 1, 2007 for the full monthly amount on the bill are qualifying payments. In addition, they must be made no later than 15 days after the due date. Only payments made while the borrower is working full-time at the qualified employer will be considered.

-

What is a qualified repayment plan?

Students who are enrolled in the Income Contingent Repayment Plan, the Income Based Repayment (IBR) Plan, and the Pay As You Earn Repayment Plan are making qualifying payments.

-

Does income influence eligibility to participate in PSLF?

Income does not affect someone’s ability to benefit from PSLF. However, income does influence the monthly payments that students make if they participate in a qualified payment plan.

-

What are the tax implications of loan forgiveness?

The Internal Revenue Service does not consider loans forgiven through the PSLF to be income. Therefore, the amount forgiven on the loan is not taxable.

-

Are student loans automatically forgiven after 120 qualified payments?

After making 120 qualified payments, borrowers must submit a PSLF application form. They must still be working for the qualifying employer in order to have their loan balance forgiven.

-

Where can graduates find more information about PSLF?

Graduates can get more information at Studentaid.ed.gov.

EXPERT SPOTLIGHT: UNIVERSITY DIRECTOR OF ADMISSIONS

Kaitlyn Tracy, Director of Admissions, Spring Arbor University

How do graduate school loans differ from undergraduate?

Graduate loans are different from undergraduate in a few ways.

Graduate students are only eligible for federal unsubsidized loans and possibly federal Grad Plus loans (which are credit based). This differs from undergraduate students, who are eligible for possibly federal subsidized loans and other loan programs, such as the Perkins Loan.

Other differences include the amount of federal loan limits available. Graduate annual aggregate limits could go as high as $20,500. Undergraduate annual limits are lower.

The lifetime federal graduate loan limit is $138,500, of which $57,500 could have been used towards their undergraduate degree.

Interest rates and origination fees could vary as well.

What advice do you offer graduate students about paying for school and taking out loans?

Choosing a graduate program is a decision that affects students for a lifetime. They should consider the following elements when choosing a program:

1. Sacrifice

A grad program is going to take time, energy, and money.

2. Save

Their savings and credit could have an impact on their ability to finance their education.

3. Seek

Financial aid by filing a FAFSA®, check local foundations, scholarship searches, military programs, education benefits from their employers, and other organizations that could be a source of funding.

4. Solicit

Help from professionals—talk to your school’s financial aid office.

5. Strategize

Based on who you are today, what your life situation is, and how much you must have to live and support yourself and your family.

What are some mistakes students make when taking out loans and how can they avoid them?

Students tend to borrow more than they need for their education. Most students take out the maximum eligibility, even if it is more than the cost of attendance. Students also do not monitor their aggregate loan amounts and are surprised when they graduate how much loan they have and what that means in a monthly payment.

The best way to avoid these mistakes is to plan ahead when enrolling in a program to minimize the amount of loans needed. Also, keep track of the total amount of loans and utilize the tools provided by studentloans.gov that can calculate their anticipated monthly payment based on their loan totals.

Additional Graduate Student Loans Resources

Graduate students can never get too much information about funding their education. Learn more about graduate school loans through some of the following resources:

Subsidized and Unsubsidized Loans

Provides a comprehensive understanding of federal subsidized and unsubsidized loans, including interest rates and repayment schedules.

Exit Counseling - StudentLoans.gov

Includes information on entrance and exit counseling, which is designed to give students detailed explanations about student loans and their responsibilities as borrowers.

Public Service Loan Forgiveness

A broad look at the Public Service Loan Forgiveness (PSLF) Program.

Federal Versus Private Loans

Students gain an in-depth understanding about the differences between federal and private student loans, and the pros and cons of each.

Interest Rates and Fees

This site includes a wealth of information on interest rates and fees, including how they are calculated and the effects they have on loan balances.